Delivery Culture Is Here to Stay

In one of the strongest signs yet of long-term changes in consumer behavior following the pandemic, food delivery services are continuing to achieve record growth even as consumers move closer to pre-pandemic levels of activity. The new era of delivery reached a milestone this month when Uber announced that delivery revenue from Uber Eats in 2021 outpaced revenue from ridesharing, Uber’s original raison d’être. Uber Eats has become the biggest delivery juggernaut globally, with presence in multiple countries and $8 billion in annual revenue, up 421% from $1.9 billion in 2019.

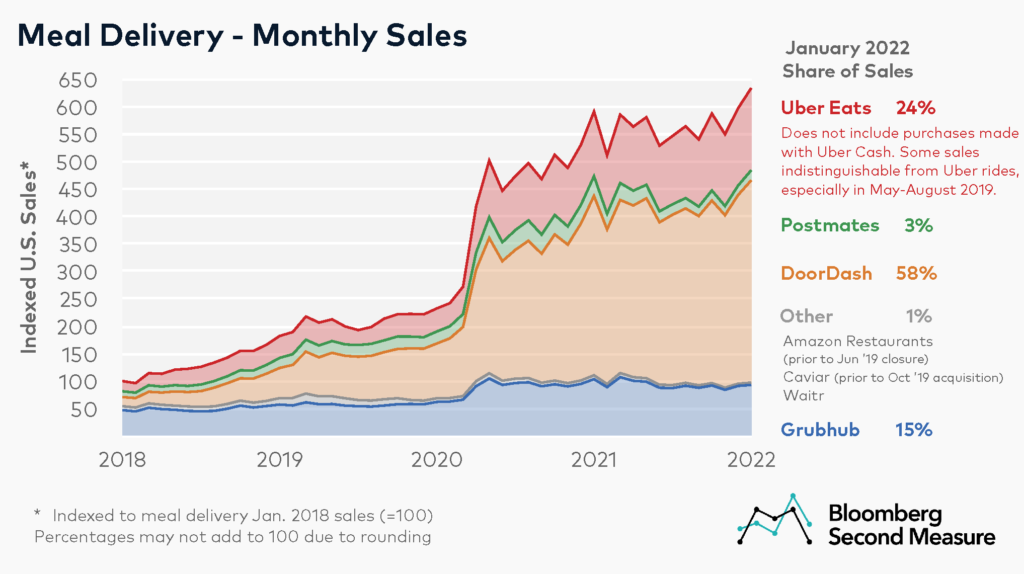

DoorDash, which had one of the most successful IPOs of 2020, continues to dominate food delivery in the U.S. with a 58% share of the market, followed by Uber Eats at 24%, Grubhub at 15%, and Uber-owned Postmates at 3%. In Q4 of 2021, DoorDash filled 369 million orders, a 35% increase over Q4 of 2020. In the words of DoorDash CFO Prabir Adarkar, “There was a lot of skepticism about whether people were going to keep using this product with reopenings, and we’re exiting the year with a record number of users. The benefit of convenience is enduring.”

Indeed, food delivery services are still winning new converts in significant numbers. As of January 2022, 51% of U.S. consumers have used a food delivery service, up from 46% one year earlier.

Some signs do point to a plateau in food delivery growth as we enter 2022. According to Yelp’s most recent Economic Average Report, consumer interest in food delivery on the platform increased only 7% from 2020 to 2021, in contrast to the huge increases of 2020, which are mostly responsible for the 107% increase in the popularity of delivery since 2019. In line with Yelp’s statistic, Bloomberg reports that overall meal delivery sales grew 7% in January 2022 compared to the previous year.

But even if growth in food delivery is slowing down, its popularity has continued to expand, this despite the fact that diners are increasingly returning to restaurants. Yelp’s report, for example, saw an increase in demand for both food delivery and in-house dining in 2021, suggesting that food ordering is not a zero-sum game. Diners want to go out more, but they’re also ordering more often from delivery services, a sign that the latter behavior has become an ingrained habit with earlier adopters and continues to spread throughout the population.

Not all pandemic commerce trends are created equal

A telling foil to delivery’s continued strength is the pandemic-aligned growth of buying online and picking up in store (BOPIS). The rise in demand for BOPIS seems, according to recent data, to have been closely tied with Covid-specific concerns, with 89% of consumers now saying they prefer home delivery, up from 80% in June 2020. According to a ChaseDesign survey last April, half of those who utilized BOPIS began doing so during the pandemic, but only half of those who had tried it planned to continue using BOPIS into the future. Some 54% of consumers said they wanted to pick out items on their own in a physical store, with some complaining that BOPIS orders were marred by quality issues, lack of availability, and longer wait times.

The contrast suggests that food delivery, which was already popular before the advent of delivery apps, fills an evergreen consumer desire for repeatable convenience when it comes to meals; in Adarkar’s words, the benefit of convenience is enduring. One might argue that apps are doing for food delivery something very similar to what Uber did for rides: upping the convenience quotient in order to make an existing service more broadly available and appealing.

Local delivery use cases grow

Looking at all of this from the perspective of local search and commerce, one can point to additional analogues. Google’s attempt to upload local inventories through its acquisition of Pointy and promotion of Local Inventory Ads can be viewed as a move toward creating a digital layer on top of local shopping, rendering the inventories of local stores available to online search just as delivery apps do for the menus of local restaurants.

As for delivery itself, its local use cases are growing. Uber launched grocery delivery in 2020 and plans to expand its grocery services in North America and Europe in 2022; the company has also made forays into local delivery of prescription medicine as well as alcohol. DoorDash, which also recently launched an alcohol service, has already made significant inroads into convenience store delivery and is currently the U.S. market leader in that category. As for groceries, DoorDash has an existing delivery partnership with Albertsons and is reputedly in talks to purchase grocery delivery and pickup company Instacart. (Walmart, whose moves to digitize its own local operations are numerous, is currently the market leader in grocery delivery and pickup in the U.S. with a 47% market share, compared to 45% for Instacart.)

Delivery apps close the physical gap between customers and nearby stores by making shopping and dining as easy as tapping a few buttons on your phone. The higher cost of delivery makes it something of an indulgence today, but ubiquity brings economies of scale. It’s quite possible that we’ll see those costs decrease over time as consumers learn to expect deliverability as a default option for local.